Disclaimer: This article is based on analysis of materials that have been publicly circulated and are disputed by involved parties. The authenticity and completeness of these materials have not been independently verified. All interpretations presented are opinions based on those materials and should not be taken as statements of fact and are presented solely for discussion and analysis. Any allegations referenced are drawn from third-party sources and remain unproven unless established through legal proceedings. Requests for correction may be submitted to support@paradoxgaming.net.

In January, when everything surrounding Ashes of Creation began to escalate publicly, many in the community expected a prolonged process toward resolution. Lawsuits appeared likely, and there was speculation that individuals, including current or former employees, might begin releasing information. One such alleged release involves what has been described by third parties as Intrepid Studios’ general ledger, which some sources have attributed to Jason Caramanis.

Caramanis is a known figure within the Ashes of Creation community. He was the subject of our previous and story video Ashes of Illusion: The Hidden Investor Behind Intrepid Studios and he has appeared via phone on NefasQS’ Twitch Show. What drew significant attention, however, was a spreadsheet that has been publicly circulated.

In his video Ashes of Creation’s Financial Records are INSANE, Nefas highlighted what he described as unusual or questionable entries within the materials he presented as the company’s financial records, including references he identified as private chefs, historical antiques, DoorDash, and company-purchased Magic: The Gathering cards. Viewers who compare the video’s claims with the ledger as presented may form their own conclusions regarding the nature of those entries, if the materials are accurate.

Based on interpretations of the ledger, some observers have suggested that the records could raise questions ranging from potential inconsistencies or classification issues to questions regarding how funds may have been categorized or separated. Nefas outlines these interpretations in his video, presenting his reasoning and citing materials he references, including the ledger, W-2 forms, and publicly referenced property records.

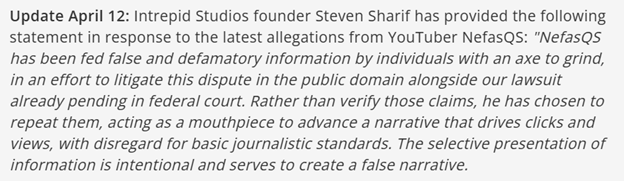

The video drew enough attention that two major gaming news organizations, Kotaku Allegations Continue To Fly Over Shutdown Of $3.2 Million Kickstarter MMO Ashes Of Creation and PC Gamer Defunct MMO studio founder denies allegation he spent Kickstarter funds on private chefs, antiques, and TCGs published coverage discussing the claims raised in the video. The following statements were reported by PC Gamer as a response from Steven Sharif to the allegations:

“NefasQS has been fed false and defamatory information by individuals with an axe to grind, in an effort to litigate this dispute in the public domain alongside our lawsuit already pending in federal court.”

“An examination of the facts through the judicial process has already revealed that the parties behind these claims orchestrated an unlawful foreclosure to take control of Intrepid’s assets from the people who built Ashes of Creation, with the intent to exploit those assets for their own benefit.”

Court records in Case No. 26CV0965 LL indicate that his motion for a Preliminary Injunction was denied. The status of the Temporary Restraining Order following the hearing is reflected in those proceedings. This article does not focus on the litigation itself, but rather is limited to analysis of the ledger discussed above based on the materials reviewed. The ledger has been described by Steven Sharif as “false and defamatory information.”

It should be noted that additional court filings related to these matters are publicly available. While those filings may provide further context, they are not the focus of this article, which is limited to analysis of the ledger discussed above.

CPAs, CFOs, and an Overview of Accounting Practices

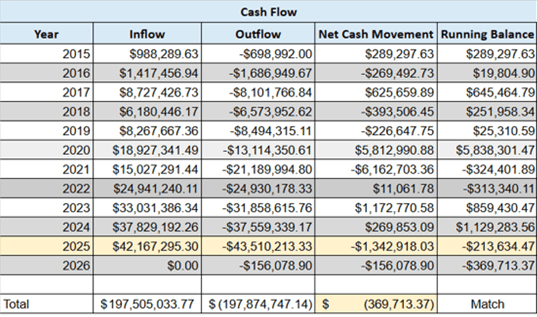

Reviewing a ledger for a company that has been active for more than ten years can be a complex task, especially when accounting codes are inconsistent or unclear. At first glance, the cash flow summary may give the impression that as much as $197,505,033.77 has moved through the records. However, based on the apparent structure of the ledger and the inclusion of internal transfers, that figure may overstate actual external cash movement and should be interpreted with caution.

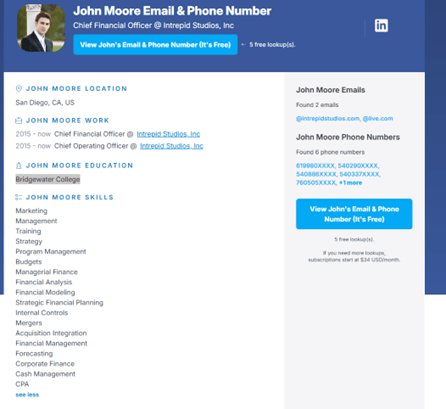

Searches of publicly accessible CPA license databases in California and Virginia conducted on April 12 and April 13 did not identify records confirming active licensure under that name. It is important to note that I am not a Certified Public Accountant (CPA), and this review is limited to publicly accessible information.

With respect to John Moore, publicly accessible records reviewed at the time of writing did not clearly confirm active CPA licensure in those jurisdictions. A document reviewed as part of this analysis includes a reference to Moore as a CPA; however, this does not preclude the possibility of licensure in another jurisdiction or under a different status.

CPAs, like attorneys, are typically required to be licensed in the jurisdictions where they practice, which involves examinations, regulatory requirements, and publicly accessible databases for verification. Financial records are not only used internally, but are subject to review by shareholders, potential investors, and regulatory authorities such as the Internal Revenue Service (IRS). If a company’s records, supporting documentation, and explanations cannot be reconciled during an inquiry, that may result in additional reviews

In the video Intrepid Studios Accounting, a high-level overview of a ledger was presented. For the purposes of further analysis, additional accounting classifications were used to better organize the data. The final column, labeled “Jahlon Accounting Codes,” reflects this independent categorization and is intended only to provide a clearer framework for reviewing the transactions, and should not be interpreted as a definitive or authoritative accounting classification.

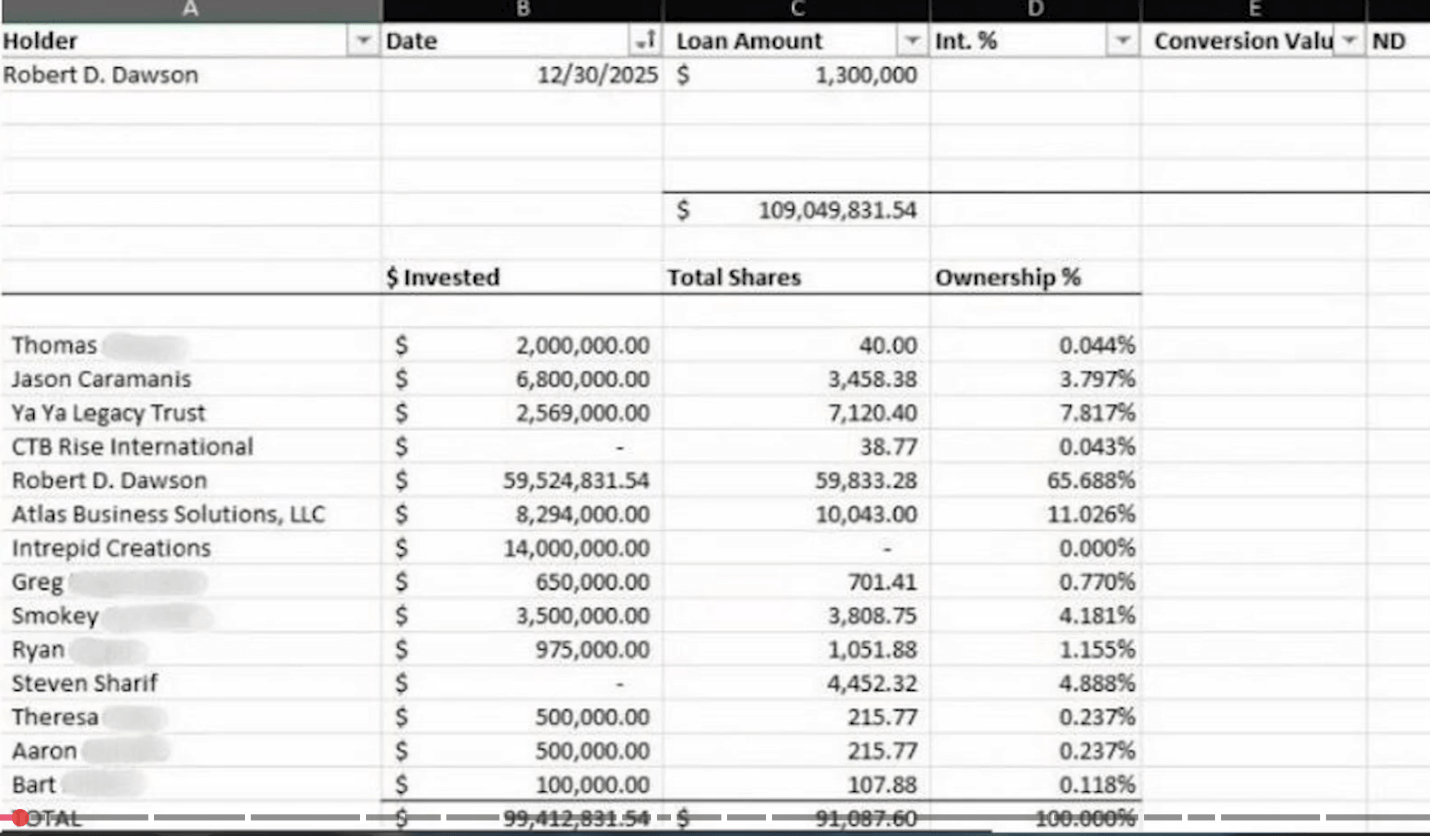

Upon initial review of the journal, there appears to be a potential difference in how the information is presented. The ledger begins with an entry of $200 categorized as “additional paid-in capital.” Separately, has been reported in documents said to have been provided to an investor and their legal representatives that he invested $9,550,000 into Intrepid Studios in May of 2015.

If both records are accurate, this may reflect differences in the timing or presentation. For example, the ledger reflects its first entry in June with a $200 balance, which may not clearly align with the larger reported investment. Without additional context, it is unclear how these figures reconcile based on the materials reviewed.

The ledger reflects an investment associated with the Alkazin transaction on September 2, 2015, followed by a $5,000 withdrawal categorized as a “shareholder distribution.” This sequence raises questions regarding how that transaction was classified and whether the designation accurately reflects the nature of the payment.

The records also reference Trek Holdings, which has been associated in some materials with John Moore. Based on the capitalization table reviewed, Trek Holdings does not appear to be listed as a shareholder. If accurate, this could raise questions as to why a transaction involving that entity would be categorized as a shareholder distribution, though additional context may be necessary to fully understand the classification.

By way of general background, Intrepid Studios is organized as a C-Corporation under California law. In such structures, distributions are typically made through mechanisms such as compensation, loans, or dividends, with dividends generally requiring proportional allocation among shareholders and being paid from retained earnings. At this stage, the company appears to have been operating on initial invested capital rather than accumulated profits, which may affect how such transactions would ordinarily be categorized.

Based on the materials reviewed, Trek Holdings has been described in some contexts as a holding entity and was listed as suspended in California records as of 2017. The ledger also appears to reflect a later transaction involving that entity in 2022. Without additional documentation, the purpose and classification of these transactions cannot be definitively determined.

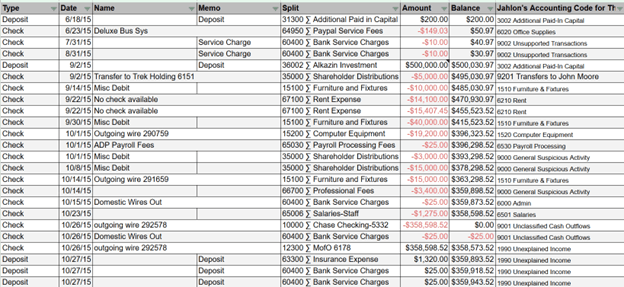

The next area of concern involves what appears to be inconsistent bookkeeping practices, which may make the records difficult to interpret without additional context.

The ledger reflects a transaction in which $358,598.52 was transferred from the Chase Checking Account (5332) to an account labeled “MofO 6178.” This type of internal movement raises questions regarding the purpose and classification of the transfer.

From a structural standpoint, repeated use of wire transfers may also introduce unnecessary transaction costs, depending on the circumstances. Additionally, the way these entries are recorded, primarily as checks and deposits without detailed supporting information, may make it difficult to distinguish between income and internal transfers.

Without clear documentation or consistent labeling, it may be challenging to determine the appropriate tax treatment of these transactions or to reconstruct their purpose at a later date.

There is nothing inherently unusual about a small business maintaining accounts across multiple banks, as this can provide operational flexibility and reduce risk if one institution experiences an issue. In some cases, businesses may separate accounts for income, operating expenses, and payroll.

In practice, transfers between accounts can be handled through a variety of methods, including ACH transfers, which may offer lower costs compared to wire transfers depending on the financial institution. The choice of transfer method typically depends on timing, cost considerations, and the specific banking relationships involved.

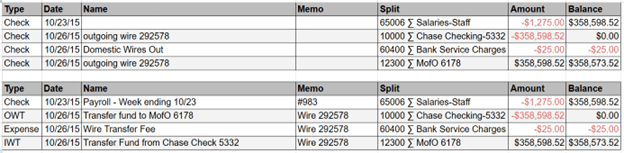

Below you will see two ledgers. The top is the ledger as it appears in the Intrepid QuickBooks, and the bottom is an alternative example illustrating a more detailed accounting structure.

In the second example, the entry includes a description indicating payroll for the week ending 10/23. The memo field also contains a reference number, which appears to correspond to a check number. These types of details can improve clarity and make it easier for someone reviewing the records, such as a CFO or comptroller, to understand the nature of the transaction.

In the remaining transactions, there is limited descriptive information accompanying the entries, which may make their purpose difficult to interpret. At first glance, several entries are labeled as checks but do not include corresponding reference numbers in the memo field, and appear to be associated with wire transfers.

In one instance, an entry is labeled as a check but reflects a positive amount, which may indicate a deposit rather than a traditional check disbursement. Without additional context or consistent labeling, it may be unclear whether certain entries represent outgoing payments, incoming funds, or internal transfers.

Inconsistent accounting practices and structure early on can create challenges later, particularly when records lack sufficient detail. Ideally, financial records should provide enough information to allow transactions to be understood without requiring significant interpretation.

One approach to improving clarity is to standardize how transactions are recorded. For example, an outgoing wire transfer (OWT) may be recorded with the destination listed in the Name field, the wire reference number included in the Memo, and the originating account identified in the split. Similarly, an incoming wire transfer (IWT) may list the source in the Name field, include the wire reference in the Memo, and identify the receiving account in the split.

Structuring transactions in this manner can serve two key purposes. First, it helps reduce the risk of misclassifying internal transfers as external inflows or outflows, as the movement of funds is more clearly documented between accounts.

Second, it improves traceability by identifying the source and destination of each transfer. This approach can make it easier to track transactions, particularly in situations where a transfer is delayed or requires follow-up, and may reduce the effort needed to reconcile account activity at a later date.

For now, this provides a general overview of the accounting structure reflected in the materials. Based on this review, the ledger may present challenges in terms of clarity and interpretation.

Some individuals associated with Intrepid Studios, including parties identified in related discussions such as Jason Caramanis and Robert Dawson, have publicly expressed concerns regarding the company’s financial management. If the records are accurate, the transactions reflected in the ledger could raise questions about the use and classification of funds, including the possibility of waste, mismanagement, or other irregularities.

The following sections highlight specific examples drawn from the materials that may warrant closer examination.

Tracking the Flow of Funds

As discussed earlier, Nefas has presented an analysis of certain transactions and expenditures highlighted in the ledger. The remaining question is how the total inflows and reported investments align with the records currently available.

In a video interview with MMORPG.com recorded on May 22, 2017, Steven Sharif stated to Robert Lashley, “In total, coming to Kickstarter, I believe I’ve put in almost $2,000,000, just about $2,000,000.”

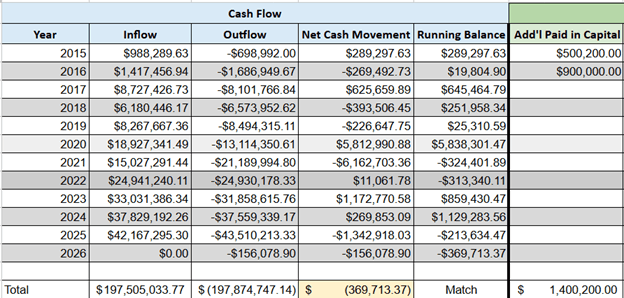

Based on a reconstruction of the ledger using materials that have been publicly circulated, the total identifiable additional capital contributions appear to be approximately $1,400,200. If accurate, this may indicate a difference between publicly stated figures and the amounts reflected in the records reviewed, though additional context or documentation may be necessary to fully reconcile these figures.

The following summary illustrates this reconstruction and provides a year-by-year view of inflows, outflows, and recorded capital contributions as reflected in the materials reviewed.

The entries shown below appear to reflect the primary deposits associated with the Alkazin investment. While the individual associated with these transactions is identified as a shareholder in the capitalization table, the corresponding ledger entries are labeled more generally as deposits, without explicit designation as equity contributions or shareholder capital.

This difference in labeling may make it more difficult to distinguish between invested capital and other types of inflows based on the ledger alone. As a result, additional documentation or context may be necessary to determine how these transactions were intended to be classified.

There is no way to determine with certainty whether Sharif contributed “nearly $2,000,000”; however, that amount does not appear to be clearly reflected in the records reviewed.

To further add context, a capitalization table attributed to Steven Sharif and reportedly provided to legal representatives of the Ya-Ya Legacy Trust indicates an investment dated May 2015. The table reflects an amount of $9,550,000 associated with that entry.

When compared to earlier public statements in which Sharif referenced contributing “nearly $2,000,000,” these figures may appear inconsistent based on the materials reviewed. Additional context or documentation would be necessary to fully understand how these amounts relate to one another.

Based on the records reviewed, there does not appear to be a clearly identifiable entry reflecting $9,550,000. Given the reconstructed cash flow analysis presented above, a variance of that magnitude would likely be noticeable; however, additional documentation or context may be required to fully reconcile these figures.

In an interview with Asmongold The WoW Killer!? Asmongold Interviews Ashes of Creation Director Steven Sharif | NEW MMORPG Steven Sharif stated:

“of which I’ve put over fifty-five million dollars of my own money into the development of this game. There’s never been a dime or profit that’s been taken from this company in eight years,”

“I am telling you that this game, that I have sunk fifty-five million or more dollars into over the course of the last eight years,”

“and will have to put in another fifty probably.”

If the figures referenced by Steven Sharif are accurate, then the reconstructed cash flow analysis discussed above would be expected to reflect those contributions. Based on the materials reviewed, total outflows appear to be approximately $197,847,747.14, with a resulting negative balance of approximately $369,713.37.

Within that framework, contributions of the magnitude described would typically be expected to be visible in the records; however, they are not clearly identifiable based on the reconstruction presented. This may indicate a difference between the available records and publicly stated figures, though additional documentation would be necessary to fully reconcile these amounts.

The following document was publicly displayed by Nefas and appears to reflect a capitalization summary in which Steven Sharif’s invested amount is listed differently. The document has not been independently verified and is presented for context only.

A central question raised by the analysis is how funds were allocated and categorized within the available records.

In prior public statements, Steven Sharif stated, “There’s never been a dime or profit that’s been taken from this company.”

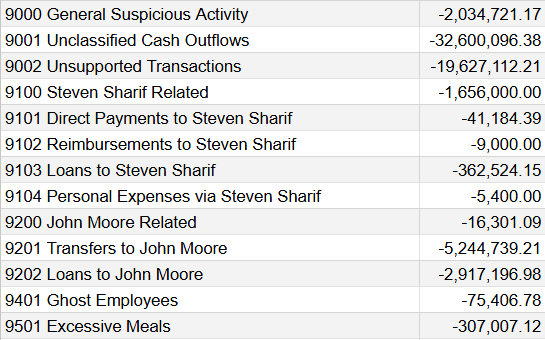

The following section reflects an independent review of the ledger conducted by PGN Media, in which transactions were grouped into categories based on their apparent characteristics within the records. These categorizations are interpretive and are intended to assist in understanding patterns within the data, rather than to serve as definitive classifications.

The summary below presents these categorized totals as derived from the materials reviewed.

The labels used in this summary are analytical in nature and do not constitute findings of wrongdoing.

Based on the categorization applied to the records reviewed, certain transactions appear to be associated with Steven Sharif, including approximately $362,000 in loans, roughly $50,000 in direct payments, and additional related expenses totaling approximately $1.6 million. Some entries are labeled in a manner that suggests connections to other individuals; however, the underlying purpose and recipients of those transactions cannot be independently verified based on the ledger alone.

Similarly, transactions associated with John Moore appear in the records, including transfers totaling approximately $5 million and loans approaching $3 million, based on the classifications applied in this analysis.

When compared to prior public statements indicating that no funds were taken from the company, these categorized totals may raise questions regarding how certain transactions are defined and whether they align with those statements. Additional context or supporting documentation would be necessary to fully evaluate these figures.

Within the categories labeled 9000, 9001, and 9002 in this analysis, the combined total is approximately $54,261,929.76 based on the records reviewed. These categories are part of the interpretive framework applied to the ledger and are intended to group transactions with similar characteristics.

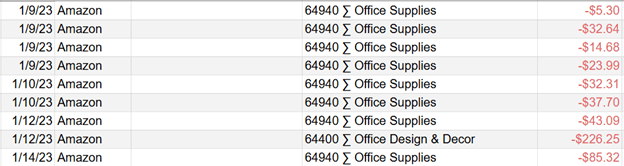

Some of these transactions may reflect legitimate business activity; however, the level of detail and consistency in the supporting descriptions appears to vary over time. In certain instances, entries such as multiple purchases from the same vendor on the same day may raise questions regarding how transactions were recorded or categorized.

While these observations do not, on their own, establish any violation, they may indicate inefficiencies or inconsistencies in recordkeeping based on the materials reviewed.

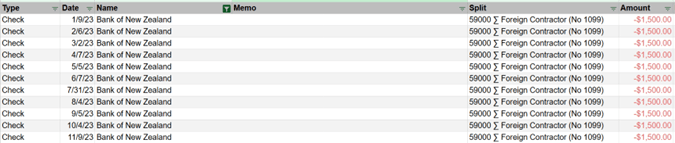

Based on the materials reviewed, the accounting entries shown above contain limited descriptive information in the memo fields. As a result, it may be difficult for an external reviewer to determine the full context of certain transactions without additional supporting documentation.

For example, the records appear to reflect transfers totaling approximately $16,500 to an entity labeled “Bank of New Zealand.” However, the entries do not include detailed references such as invoice numbers, account identifiers, or other contextual information that would clearly explain the purpose of these transactions.

Another observation is that corresponding wire transfer fees are not readily identifiable alongside the transfers to the Bank of New Zealand based on the records reviewed.

In general, similar transfers may be expected to include associated fees depending on the financial institution and transaction type. Without additional documentation, it is unclear whether such fees were incurred, recorded elsewhere, or structured differently in the ledger.

Based on the materials reviewed, the accounting records raise a number of questions regarding how transactions were recorded and classified. As of April 14, 2025, additional information has continued to emerge, and further analysis may provide additional clarity over time.

This article is intended to highlight observations drawn from the available records, though many aspects remain unresolved and may require further documentation or review to fully understand.

Additional coverage and analysis may follow as more information becomes available.

No conclusions regarding wrongdoing are made in this article. The purpose is to examine and organize publicly circulated materials for discussion.